Two Minute Drill--February 23

Share counts and security blankets

Share counts and security blankets

We like to consider share counts in our thinking about a stock investment, even in a relatively short time-frame. Lower share counts should, all other things being equal, reduce bad negative earnings surprises. After all, if a company has the cash to buy back shares they are likely to be doing something consistently right, and a disappointment in earnings numbers might be more communication nuance than serious trajectory problem.

We focus on three sectors when considering this—financials, energy and tech. And while we look primarily to marry an investment thesis with price validation, a declining share count serves as a security blanket that sudden downdrafts in a stock due to unanticipated negative events that are specific to the company are less likely.

Just as the energy sector finally got religion about returning cash to shareholders after a long period of pursuing production growth above all else, the large cap part of the tech sector may turn to capital discipline in a more rigorous way eventually. Sharing some of the gushing cash flow from a large tech company with shareholders we would guess will lead to less volatility in the sector over time and lead to less concerns about over-valuation during periods of sharp price appreciation. If we weren’t talking about AI, we think this would be an area of focus for tech in general.

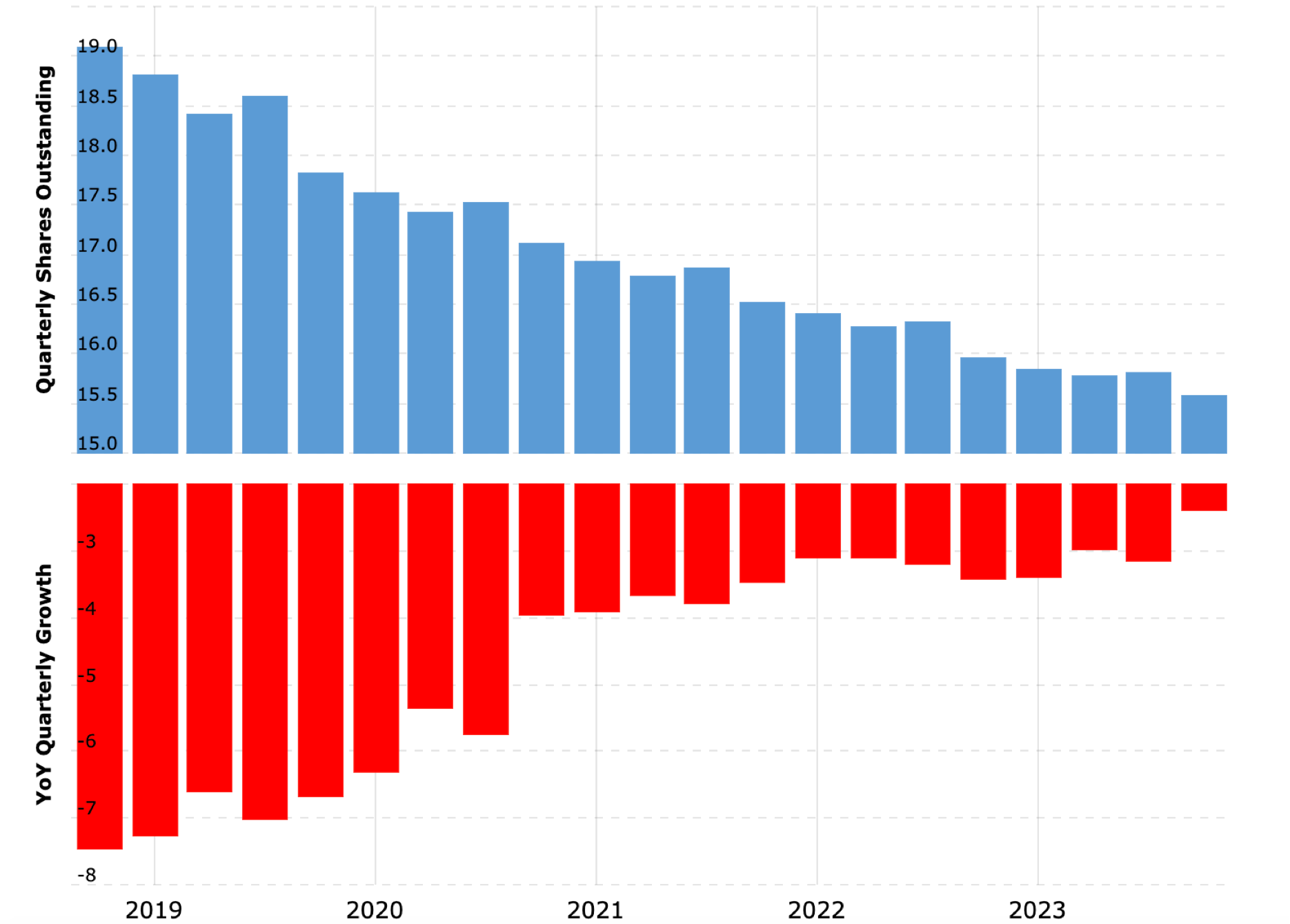

This is Meta’s share count over the past five years:

That’s impressive! While stronger investment into AI might slow share count reduction at some companies, we think it is starting to be something shareholders want to see out of large cap tech just as they did from energy companies as the opportunities for growth matured. Here is GOOG:

And AAPL is an interesting case—where share count reduction has started to decline rather sharply—maybe a factor behind lagging the other companies of the Big 7?

Citi: One of our focus holdings is Citi. We believe in the restructuring story, and we think it will lead to better cash flows to shareholders. The last bar in this chart, we think, suggests that is happening:

But mostly we believe because the market has (finally) started believing:

Is there room to go for Citi? There absolutely is, if the bank gets re-rated to its peer large cap banks in the US: