Two Minute Drill--February 21

Narrative "friction"

Narrative Friction

When the market is stretched after a long run, either up or down, eventually you begin to get friction in the narrative that is driving the price action. This friction might be introduced to little market reaction but then other friction begins to occur. For this cycle, it has been the market pricing of rate cuts going from six to three in a short period—that didn’t seem to get much attention in the equity market. Then a hot CPI print, continued strong economic news, rising long bond yields—adding up. No dramatic market reaction to any individual piece. And lastly the AI bubble pinpricks. Eventually the accumulation of friction results in slowing, and then turning the market direction.

That seems to be where we are now—almost regardless of what happens with NVDA earnings tonight. And by “what happens” we mean the market’s reaction, not the actual numbers which will undoubtedly be strong.

We are playing NVDA conservatively bearish, with a bear call credit spread that has to hit 850 for us to lose money expiring Friday (put on last week), and one that has to hit 800 for us to lose money expiring next Friday (put on yesterday). And we will take it from there after the numbers.

After a 57% rise in six months, this seems like a rational response as earnings draw nearer—resistance to a further rally, and then some profit-taking in front of the number.

You have probably seen Palo Alto Network’s soft earnings reaction (PANW) down 22% in pre-market. But it is also taking cybersecurity peers ZS and CRWD with it. Both are down nearly 9% and report earnings in coming weeks. Broader corrections seem in store with any stumble in a sector-specific name.

It is interesting that the tech sector over the past month has under-performed the S&P already by a significant margin.

LLY is down nearly 2% pre-market after a fall yesterday. This looks like it is due for a correction as well.

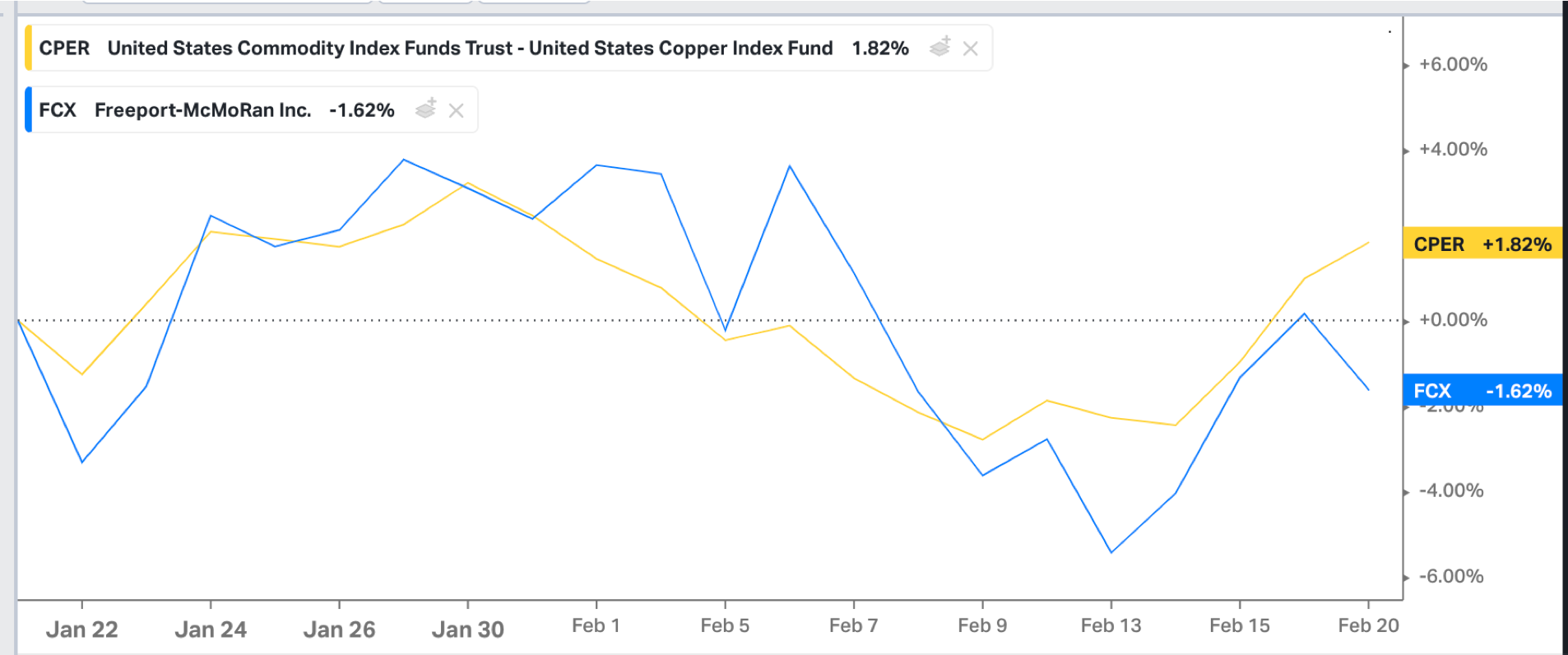

Copper is recovering, up nearly 6% in the past five days and 3.5% in the past month, but large cap copper producer FCX has lagged the move pretty significantly. Seems like an opportunity. We are long FCX.

Has AAPL gotten tired of falling? Bit of a rally later in the day yesterday, and flattish to green in the pre-market.

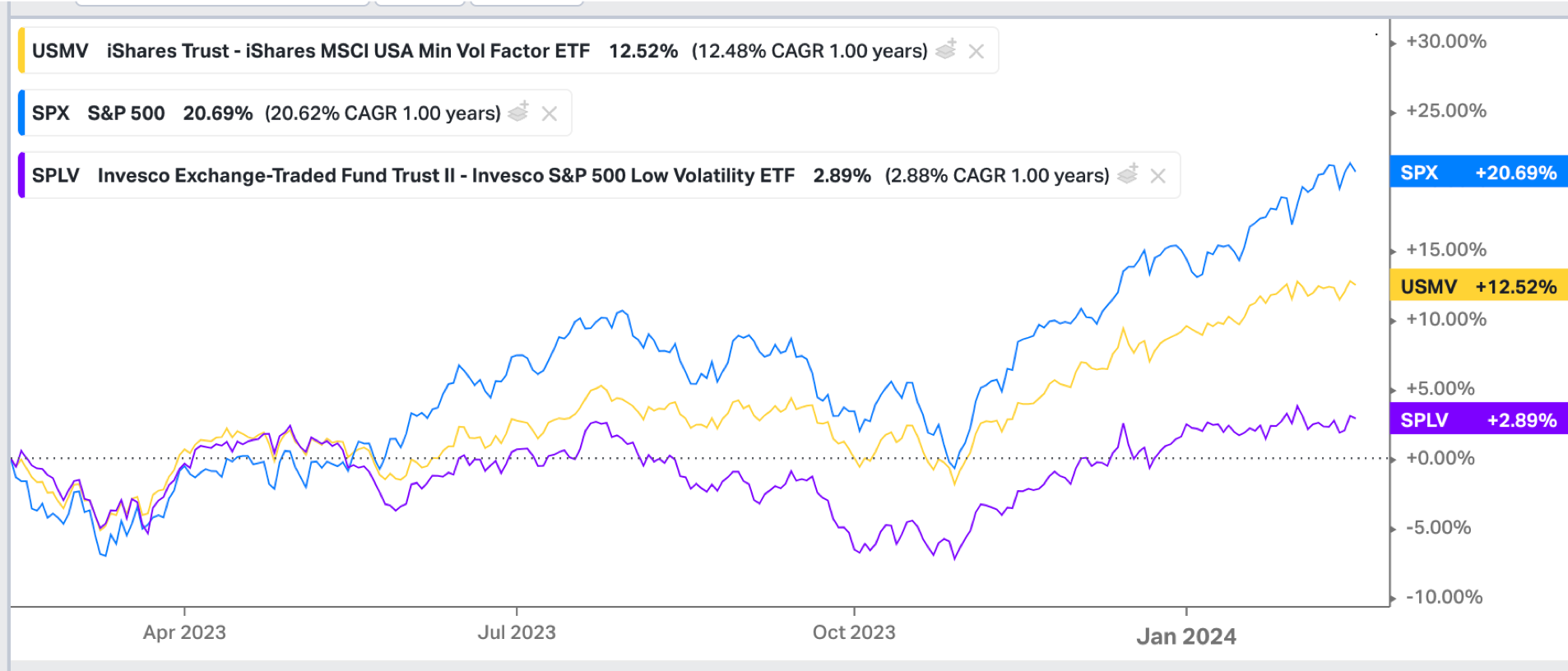

One of the hardest things for financial advisors and others to do with ETFs is play the “factor” game. There is a wild divergence in performance of various ETFs no matter which factor you choose.

In our view, it is better for the average fiduciary to tilt portfolios with sector weightings if that is the desire rather than choose a factor in an attempt to out-perform the market. Because not only must you choose the correct factor, but the correct ETF purportedly representing that factor to do well.

Below is an example if you were to choose a minimal volatility factor because you believe we are going into a correction. At the end of the day, simplicity in expressing a view has a high probability of producing an optimal result.